Building Better, Bigger, and Broader Portfolios for Long-Term Compounding

Over the long run, the chart of stock prices traces a graceful line from the lower left to the upper right—a powerful illustration of wealth compounding. But zoom in to the scale of a typical human lifetime, and that smooth climb reveals wild market swings and deep drawdowns. None of us can choose the era in which we invest—or whether luck places our timeline on the steepest, smoothest stretch of that curve.

The real driver of compounding wealth, however, has less to do with luck—or complex finance—and far more to do with the arithmetic of steadily growing capital. Volatility, drawdowns, and taxes all conspire against this growth. Resilience against these forces requires a more thoughtful, institutional, and modern approach. Portfolios designed to navigate real-world market cycles and enhance long-term compounding need to be built Better, Bigger and Broader.

The Foundation: Better Portfolios Through Meaningful Diversification

A better portfolio delivers stronger returns for the level of risk taken—producing a more favorable risk-reward tradeoff. Portfolios composed only of stocks and bonds can fall short, especially during periods of market stress when both asset classes may move in the same direction. True diversification means adding assets or strategies that behave differently across a range of economic environments, improving portfolio outcomes by tapping into return streams that are less correlated with traditional holdings.

Among these, systematic strategies, such as managed futures and trend-following stand out. They capitalize on price movements across a wide range of global markets, including many that traditional portfolios ignore. Their returns are largely independent of both stocks and bonds, and they tend to perform particularly well during extended market downturns. Adding uncorrelated strategies like these meaningfully improves diversification and the overall risk-return profile—making the portfolio better.

Most portfolios lack these strategies and other beneficial assets because they either fall outside conventional allocations or because many advisors lack the tools or expertise to implement them well.

Scaling Smarter: Bigger Portfolios with Capital Efficiency

Meaningful diversification improves a portfolio by reducing overall risk—lowering both the up-and-down swings (volatility) and drawdowns. However, part of what makes the portfolio better can also limit it: allocating to diversifying assets often means reducing exposure to traditional return drivers like stocks. While risk may decline substantially, returns can dip slightly—resulting in a more efficient portfolio, but one that may fall short of an investor’s original return goals.

The solution is to make the portfolio bigger: scale exposures to preserve the improved risk-return balance while targeting higher returns. This is not about indiscriminate risk-taking, but about disciplined use of tools – like capital efficient funds – to preserve exposures.

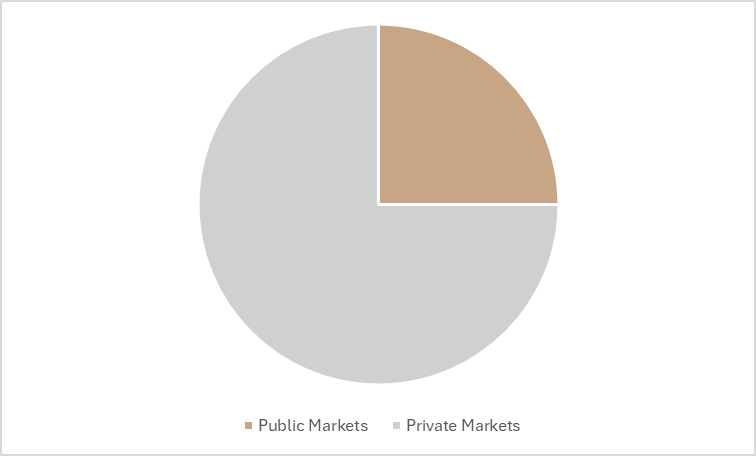

Expanding Access: Broader Portfolios with Private Markets

“Better” and “Bigger” portfolios can be built entirely within public markets, but accessing a wider opportunity set of assets and strategies can enhance returns and improve diversification. Private markets—once the exclusive domain of pensions, endowments, and other institutions—are now increasingly accessible to individual investors and represent a compelling opportunity for many portfolios. Broadening a portfolio means including private market investments—assets not traded on public exchanges—such as private equity, private credit, private real estate, and infrastructure. These investments should offer an illiquidity premium, compensation for lack of immediate access to your investment, but that’s only part of the story. They tap different areas of the economy and markets, provide unique drivers of return, and offer additional sources of diversification that can help reduce overall portfolio risk. Sized appropriately, they play a powerful role for many investors—enhancing long-term growth, improving resilience, and building a more well-rounded foundation for compounding.

Preserving Growth: Tax-Aware Strategies for Long-Term Compounding

Markets drive growth, but taxes quietly erode it. Tax strategy must be embedded from the start—not added as an afterthought. This includes not only placing the right assets in the right account types based on their tax characteristics, but also taking advantage of new opportunities to harvest losses, optimize capital gains treatment, and use innovative structures that can defer or potentially eliminate taxes. These techniques represent the frontier of tax-aware investing. Integrated thoughtfully, they can significantly improve the returns investors keep—preserving wealth and accelerating long-term compounding.

A Holistic Framework

Compounding wealth is not about chasing returns or predicting the future. It is about preparing portfolios for whatever comes next. The strongest portfolios are Better, Bigger, and Broader: thoughtfully diversified, efficiently scaled, and expansive enough to capture a wider range of opportunities.

- Better portfolios improve the risk-return balance through true diversification.

- Bigger portfolios use capital efficiency to scale those improvements and target higher returns.

- Broader portfolios expand the investment universe beyond public markets, unlocking new return drivers and deepening resilience.

This holistic framework is designed to help investors withstand market turbulence, stay invested through cycles, mitigate taxes, and grow wealth with more confidence. Whether you’re revisiting your investment strategy or laying the groundwork for the first time, this framework offers a clear foundation for building portfolios—and what you can expect as we move forward together.

Sources:

Stocks: VTSMX (Vanguard Total Stock Market Index Fund),

Trend following: SG Trend Index (SocGen Trend Index).

Portfolios are rebalanced annually. Returns, volatility, and drawdowns based on end of month values.

Equity drawdown periods:

Tech Bubble: Oct 2000 - Sept 2002

GFC (Great Financial Crisis): Sept 2007 - Feb 2009

2022 Rate Hikes: Jan 2022 - Sept 2022

Disclaimer: The opinions voiced and information provided in this document is for informational and educational purposes only. It should not be considered investment, financial, or legal advice. Nothing herein constitutes a recommendation to buy, sell, or hold any security or financial instrument. Magnolia Private Wealth does not provide tax, legal or accounting advice. Investing involves risk, including the potential loss of principal. You should consult with a qualified financial advisor, tax professional, or other appropriate professional before making any financial decisions. The author and publisher assume no liability for any losses or damages resulting from the use of this information.

Insights from Our Team.