The Enemies of Compounding

The beauty of compounding lies in its simplicity: gains on gains over time. But in the real world, that process gets interrupted. Three persistent forces work against its progress:

- Volatility (up-and-down swings)

- Drawdowns (large losses)

- Taxes

Together, they quietly conspire to slow—or even reverse—wealth creation.

Volatility: The math doesn’t favor a bumpy ride

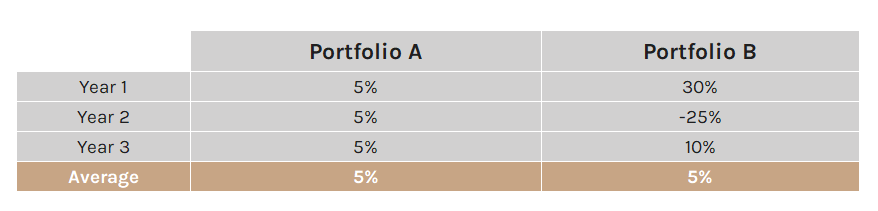

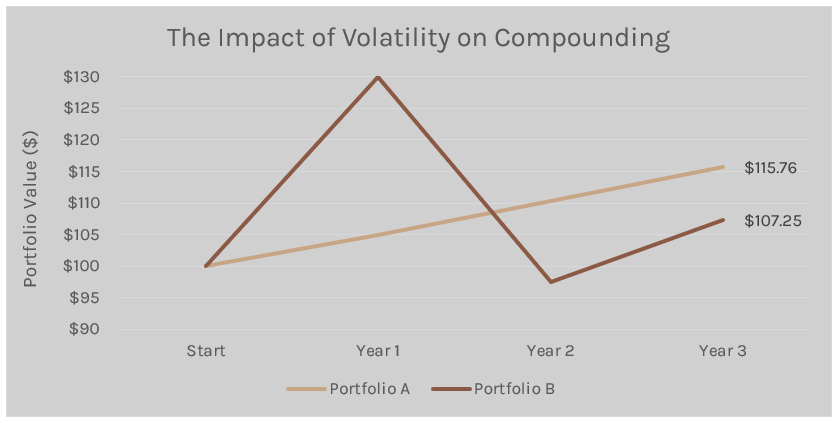

Consider two portfolios over three years:

Both Portfolio A and Portfolio B average 5% per year. But the Compounded Annual Growth Rate (CAGR)—what you actually earned on each dollar invested—tells a different story:

- Portfolio A: 5%

- Portfolio B: 2.36%

In other words, Portfolio B’s higher volatility reduces its effective returns by more than half. That’s volatility drag. It’s not theoretical—it’s arithmetic.

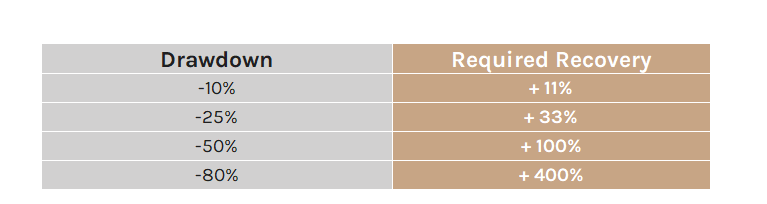

Drawdowns: The deeper the loss, the harder the recovery

Large drawdowns may be the single biggest headwind to compounding. And real-world investors have faced many:

- Multiple 50%+ drops: this century alone has seen steep stock market declines of 50%+ during the Dot-Com Bubble (2002) and the Global Financial Crisis (2009).

- Several significant declines over 20%: recently including the COVID Crash (2020), the Fed rate-hiking cycle (2022) and tariff concerns (2025).

- Extreme downturns: some markets suffered even deeper losses: for example, the Nasdaq tumbled over 82% when the Dot-Com Bubble burst.

These major drops often come on the heels of periods of surging prices and optimistic headlines—exactly when everyday investors tend to pile in– making the eventual plunge even more devastating.

Compounding relies on keeping capital intact but returns are asymmetrical, a loss hurts more than a gain of equal magnitude helps. Even worse, if you need to withdraw funds when your portfolio is already down, a portion of the losses is irrecoverable.

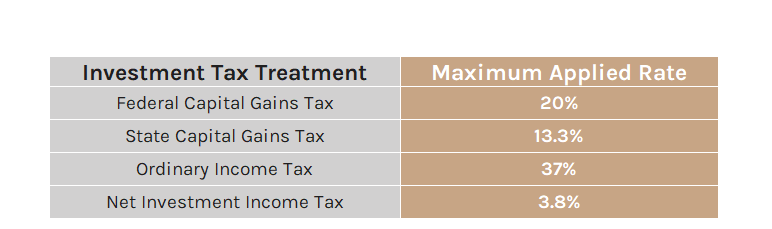

Taxes: The (almost) unavoidable drag:

Every dollar claimed by your silent partner—the Government—is a dollar that never gets a chance to grow on your behalf. Like volatility and drawdowns, taxes erode compounding by siphoning away returns before they even have a chance to materialize. In high-tax states, federal, state and local levies can chip away as much as 50% or more of your investment gains, delivering a significant blow to long-term compounding.

At Magnolia, we design portfolios that account for these real-world frictions—volatility, drawdowns, and taxes—not ignore them. We build portfolios that are better by being more resilient, with strategies that reduce drawdowns and smooth volatility. They’re structured to offer stronger risk-reward tradeoffs without sacrificing long-term goals. And they’re built with tax-awareness from the start—in composition, structure, and ongoing strategy—so more of your capital stays invested and compounding.

The goal is simple. It’s about removing the obstacles that stand in the way of compounding—and giving your wealth the clearest path forward through every cycle.

Disclaimer: The opinions voiced and information provided in this document is for informational and educational purposes only. It should not be considered investment, financial, or legal advice. Nothing herein constitutes a recommendation to buy, sell, or hold any security or financial instrument. Magnolia Private Wealth does not provide tax, legal or accounting advice. Investing involves risk, including the potential loss of principal. You should consult with a qualified financial advisor, tax professional, or other appropriate professional before making any financial decisions. The author and publisher assume no liability for any losses or damages resulting from the use of this information.

Insights from Our Team.