From the Frontier: Long/Short Extensions

The value of tax-loss harvesting has a ceiling. In rising markets, losses dry up, cost basis rises, and the strategy that once generated meaningful offsets quietly stops producing. The result is a portfolio that was built to be tax-efficient and no longer delivers.

Long/short extensions are a different tool altogether. They generate realized tax losses–systematically and in any market environment–while at the same time targeting returns above the benchmark. They accomplish what traditional tax-loss harvesting approaches were never designed to deliver: shrinking a concentrated stock position without triggering a tax event, absorbing the gains from a business or property sale, or unlocking a portfolio that has become too appreciated to manage efficiently.

What They Are

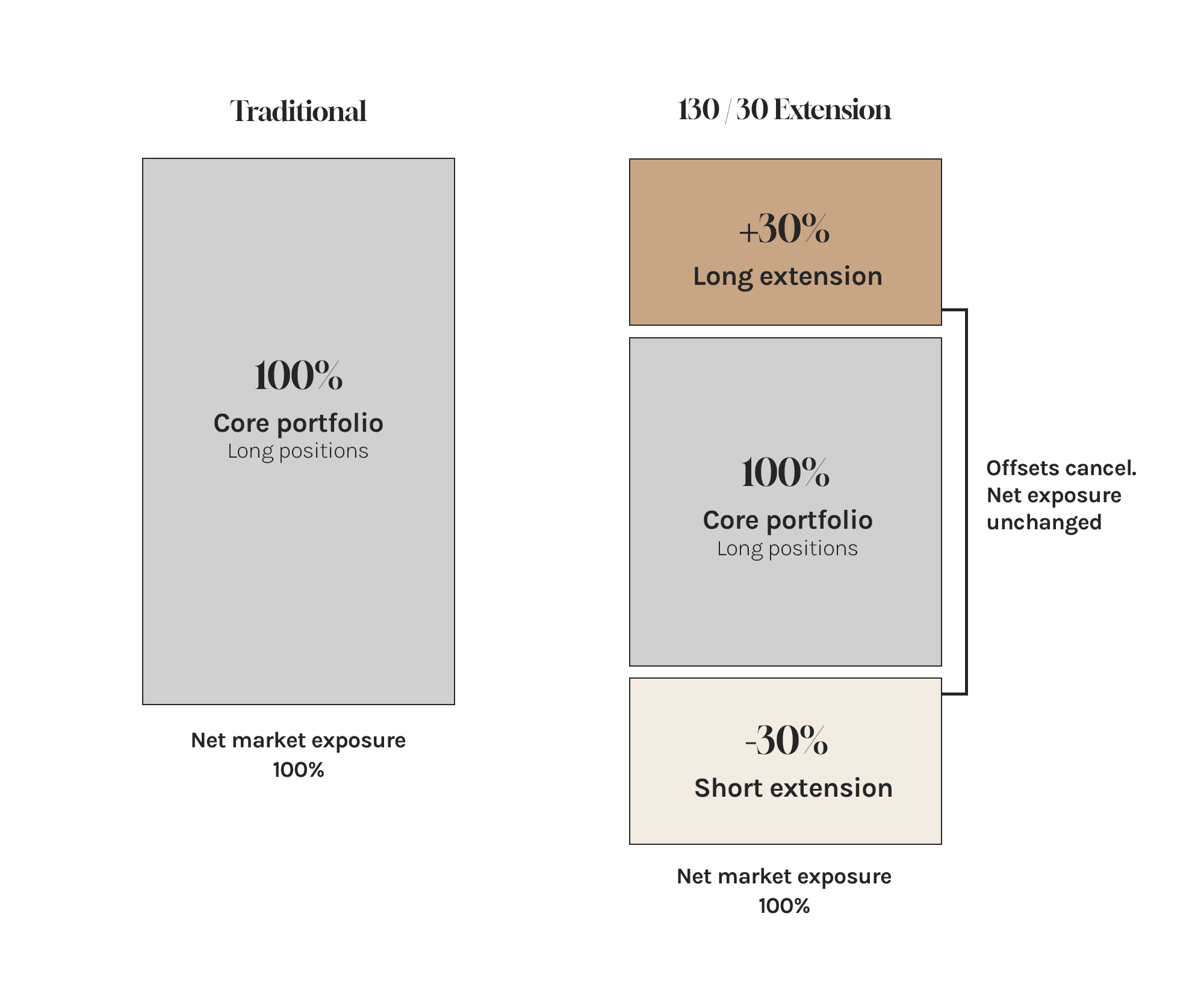

A long/short extension is an overlay added to your existing portfolio or cash, managed by institutional firms with sophisticated risk controls and substantial computing infrastructure. The strategy holds additional positions in stocks expected to outperform and simultaneous bets against stocks expected to underperform–relative to a broad market benchmark like the U.S. or global equity market. Because long and short positions offset each other, net market exposure stays at 100%, your exposure to broad market movements doesn’t change.

The most common configuration adds a 30% extension of additional positions and a 30% short extension on top of a 100% core — referred to in shorthand as 130/30. The extensions can be sized up or down depending on the investor's objectives, risk tolerance, and the magnitude of capital gains you need to offset. Larger extensions generate more losses and more potential outperformance, with commensurately more tracking error and cost. The extensions can also be constructed to offset existing concentrations — too much in a single sector, for example — using the short side to reduce that weight while loss harvesting runs simultaneously. For cash-funded accounts, the total portfolio exposure can be calibrated to be fully invested in the market, partially invested, or market-neutral.

In a traditional portfolio, losses can only be harvested when stocks fall. Add a short extension, and rising stocks generate losses too: a short position loses money when its stock goes up. The result is a portfolio that continuously produces harvestable tax losses–in up markets and down–without any corresponding economic loss.

The mechanics of the portfolio are systematic. The managers running these strategies oversee tens of billions in assets and have run long/short equity strategies for decades — institutional infrastructure now made available to individual investors. The entire investable universe of stocks is ranked on favorable characteristics–called factors– like value, momentum, quality, and earnings reliability. The manager adds the strongest expected performers to the portfolio and bets against the weakest. Prices of individual stocks move independently, creating a steady stream of positions with embedded losses that are sold, replaced with similar securities, and recycled. Tax losses are locked in. Economic exposure is maintained and the strategy runs continuously.

The Tax Benefit

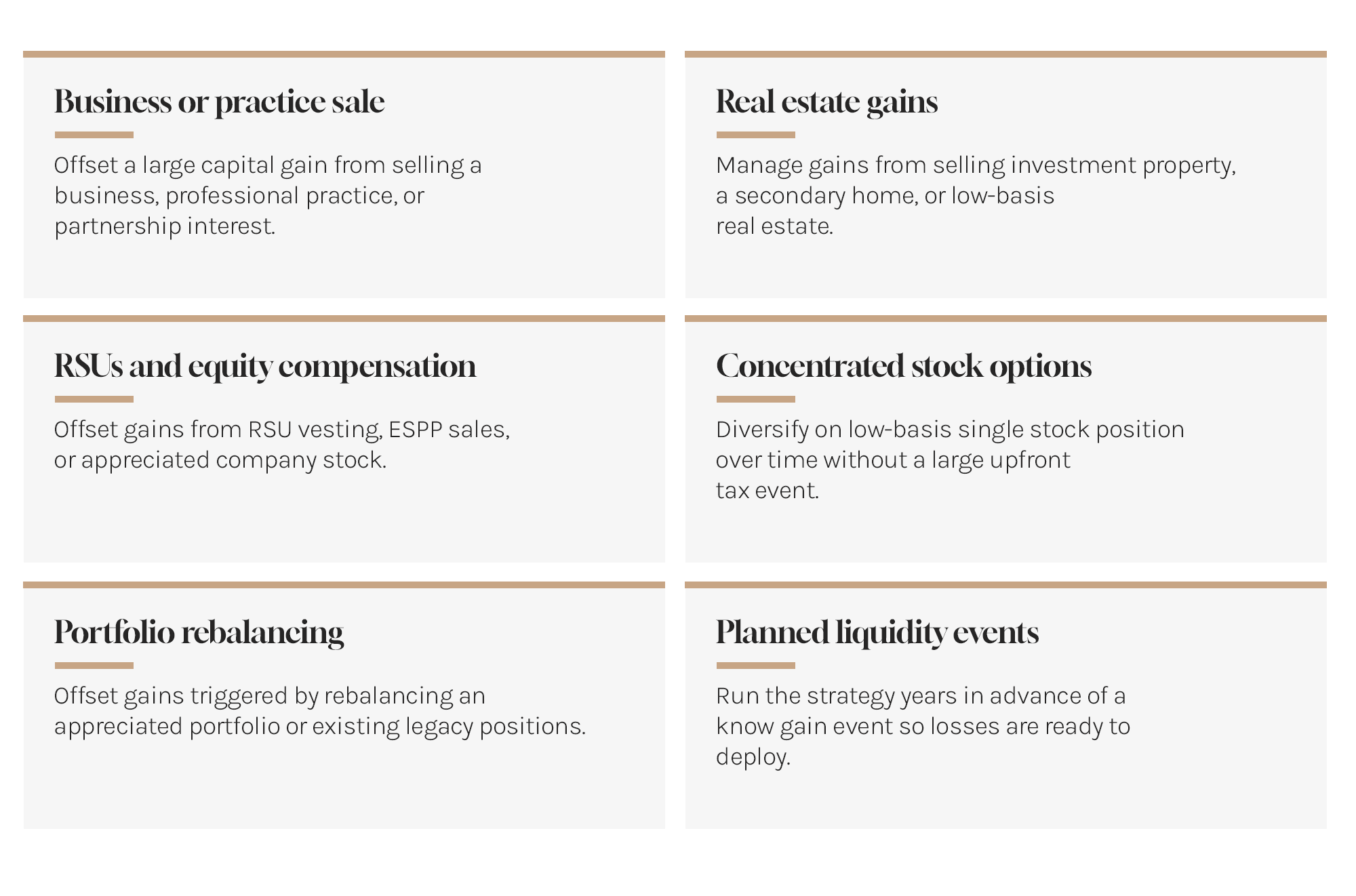

The primary output is realized capital losses that offset capital gains dollar-for-dollar on your tax return. These are not losses in your portfolio; the portfolio is designed to track a benchmark. Capital losses are the purpose of the strategy, not a cost. Common applications include but are not limited to:

Common Applications

The losses generated are mostly short-term in nature and offset short-term gains first. Those gains would be taxed at ordinary income rates as high as 40.8% at the Federal level when we include the net investment income tax. Any additional losses will offset long-term gains, which are taxed up to 23.8%. State taxes can push both rates meaningfully higher. Losses in excess of all gains offset up to $3,000 of ordinary income each year, and can be carried forward indefinitely. Taxes deferred today is money compounding in your portfolio tomorrow and all future days. And if assets are held until death, a step-up in basis can make a deferred tax an eliminated tax.

Loss generation is front-loaded in the early years, but continues to generate consistent losses in perpetuity. Therefore, it pays to embark on these strategies well in advance of any known taxable gain event — a business sale, a property transaction, or a liquidity event that may be years away. The losses accumulate, are carried forward, and are ready to deploy when they are needed most. Over time, those accumulated losses can also be used to fund tax-efficient withdrawals from the portfolio itself — taking money out each year without triggering a tax bill.

What it Costs and What You Get Back

These strategies come with costs: margin interest on the additional long positions, stock borrowing fees on the short side, and manager fees. All-in, costs of a standard 130/30 configuration typically run 0.75–1.0% annually, depending on the manager and leverage level. The interest expense itself is tax deductible, which reduces the net cost meaningfully for high-bracket investors.

These should not be confused with passive strategies which aim for index returns minus fees and expenses. The managers we partner with apply sophisticated stock selection, designed to generate excess returns above the benchmark, on both sides of the portfolio (“alpha”). This alpha aims to more than offset the cost of the strategy over time — meaning the net return objective is benchmark-plus, not benchmark-minus — before accounting for the tax benefits.

Tracking Error and Risk

Active management creates tracking error — the degree to which the portfolio's return can stray from its benchmark in any given period. This is a feature, not a bug. At a standard 130/30 configuration with a 1.5% tracking error target, if the benchmark returns 12% the portfolio will return about 10.5% to 13.5% most years. At higher leverage levels, that band widens, as does the potential alpha and the tax benefit.

Tracking error is a necessary feature of active management. It will add to performance relative to the benchmark some years, and subtract in others. But over time, these strategies are designed to deliver above-benchmark returns–and enough to cover fees and expenses.

Unwinding a Long/Short Extension

Long/short extensions are designed to deliver strategic long-term economic value. Over time, realized losses accumulate alongside embedded unrealized gains in the extensions themselves. When it comes time to reduce or exit the strategy — whether because the tax objective has been achieved or circumstances change — how the unwind is managed matters considerably.

Done gradually over multiple years, managers can use currently generated losses and accumulated loss carry-forwards to offset embedded gains as they are realized, releasing capital back to the investor with little-to-no tax liability. If the unwind is done hastily, a large portion of the deferred gains will be crystallized at once. Larger extensions require a longer runway to unwind efficiently, and the initial decision to use a long/short extension should take this into account.

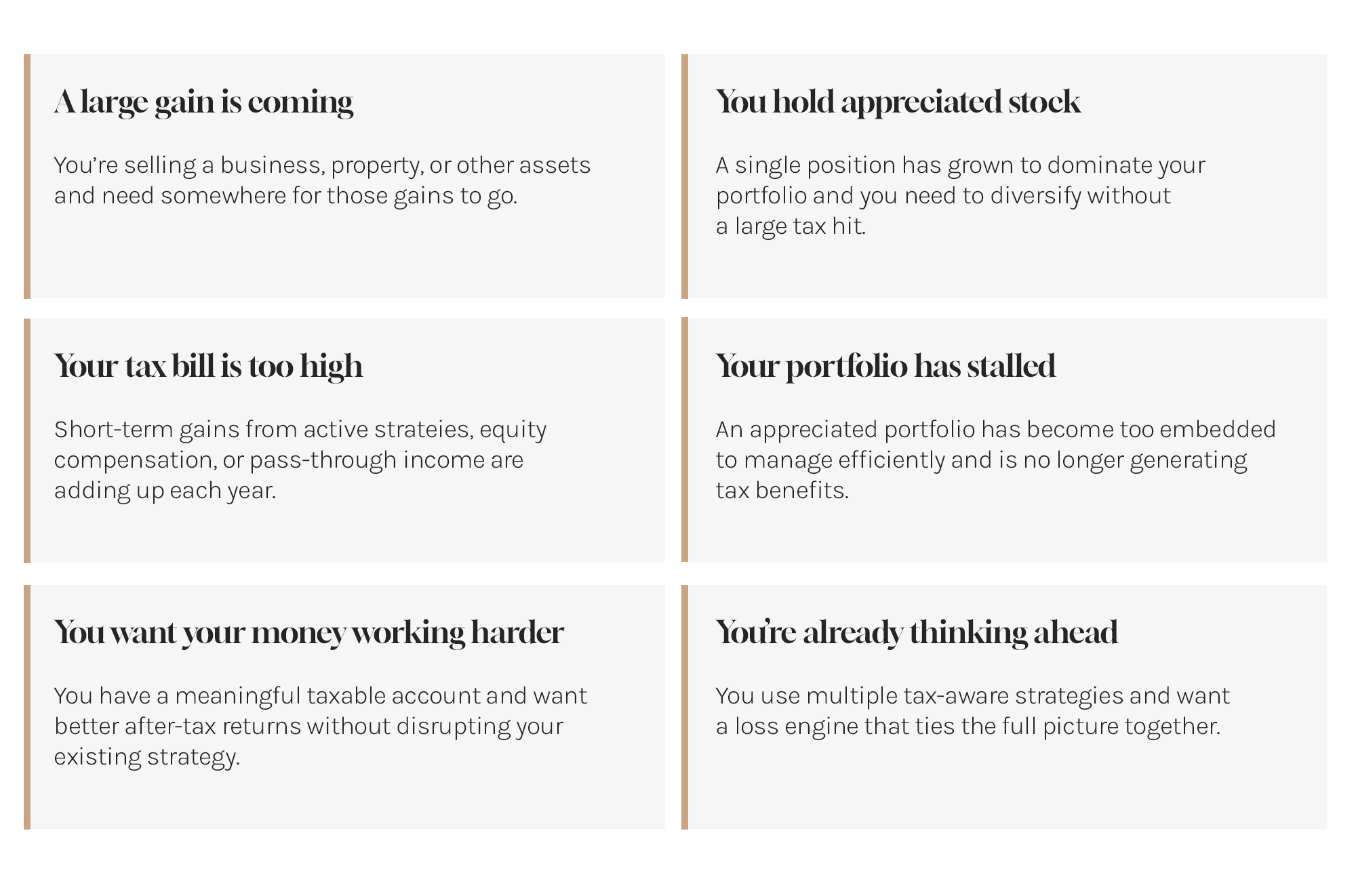

Who This Is For

Long/short extensions are not the right tool for every investor, but they are useful to more investors than you might think. The only requirements are a large-enough taxable account and a willingness to embrace a modest degree of active positioning. If these are met, the applications are very broad.

Many of our clients use multiple strategies from the Frontier of Tax-Aware Investing. For those clients, long/short extensions typically serve as the loss engine that powers the broader portfolio — generating the realized losses that allow each strategy to work more efficiently and the combined tax benefits to compound in their favor.

Investors with substantial taxable assets usually have capital gains elsewhere and those gains are rarely managed as efficiently as they could be.

These strategies generally require a minimum account size of $1 million. Our early engagement and ongoing relationships with leading managers of these strategies has already saved our clients hundreds of thousands of dollars in taxes, and we have been able to achieve flexibility on minimums in some cases. If you’re not certain you qualify, it is worth a conversation.

How It Works in Practice

These strategies use separately managed accounts (SMAs) — individual accounts held in your name at a major custodian like Fidelity or Schwab. Every position is visible, every tax lot is tracked, and losses are reported on the same Form 1099 you receive each year: it’s simple, transparent, and won’t slow down your CPA at tax time.

Magnolia's Advisory Role

The most effective use of these strategies depends on a number of factors, and an advisor with the right experience can help find what’s right for you: whether they make sense at all, how much leverage to take on, which assets to fund these strategies with, which capital gains events to prepare for–then integrated with the entirety of your tax situation and your financial plan. Thoughtful coordination, with the help of an advisor who understands all of these facets of your financial life, is where most of the value is created or lost.

We have spent considerable time vetting managers, evaluating custodial infrastructure, and working through the detailed mechanics of these strategies. We understand all this as well as anyone, and are able to confidently tell you whether it makes sense for you, and how to proceed if it does.

If you are facing a meaningful capital gain event, or simply want to understand whether your current portfolio is working as hard as it could on an after-tax basis, we strongly recommend you consider this strategy.

Disclaimer: The opinions voiced and information provided in this document is for informational and educational purposes only. It should not be considered investment, financial, or legal advice. Nothing herein constitutes a recommendation to buy, sell, or hold any security or financial instrument. Magnolia Private Wealth does not provide tax, legal or accounting advice. Investing involves risk, including the potential loss of principal. You should consult with a qualified financial advisor, tax professional, or other appropriate professional before making any financial decisions. The author and publisher assume no liability for any losses or damages resulting from the use of this information.

Insights from Our Team.