When It Rains, It Pours

Ten-dollar umbrellas might sell for twenty in a downpour, so it’s better to buy them when the sun’s out. “Fair” is just a matter of opinion: supply and demand set the price no matter the weather. The same is true of financial assets.

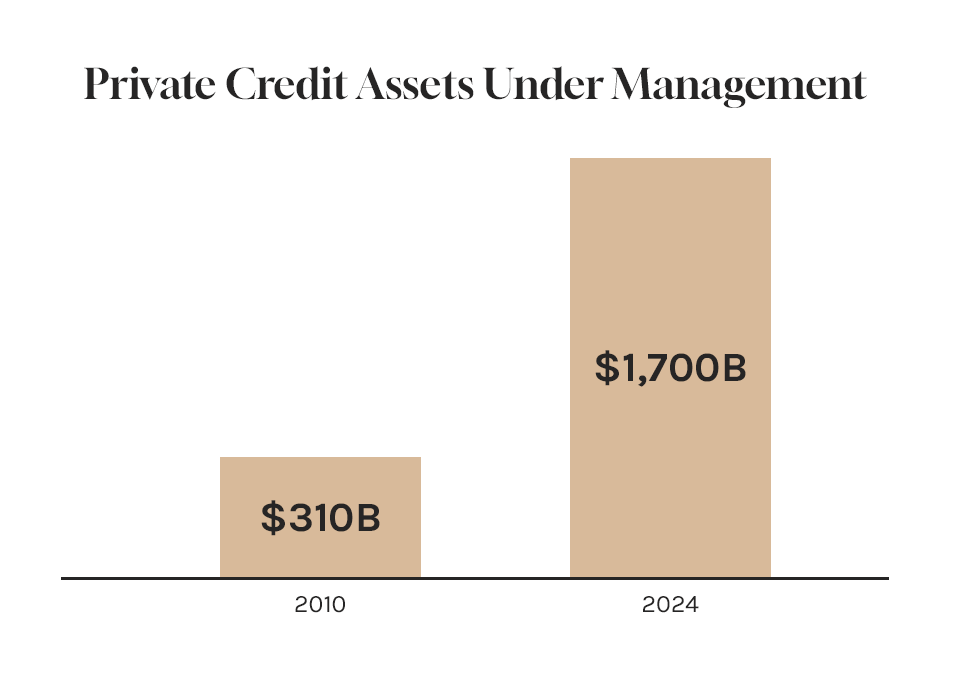

Consider the plight of the banks. The regulatory shadow cast by the Great Financial Crisis cooled traditional lending activities and reduced the supply of loans. This meant higher interest rates for borrowers. But capital markets adapt and private lenders have since rushed to fill the void. Now banks are clawing their way back into the arena and competition has heated up. More supply means lower interest rates for borrowers and lower returns to investors.*

Every loan needs a borrower. In private lending, more demand for loans requires more private equity ownership, more mergers and acquisitions, and more public listings. These have been scarce in the last few years.

For the investor, weak demand and excess supply lead to lower returns: the lender has to offer a lower rate and will tend to loosen lending standards to get money out the door. The investor gets a lower return and takes more risk.

What could go wrong? We’ve seen this dynamic play out on a massive scale as the root cause of the Great Financial Crisis. Global demand for safe assets inspired Wall Street to supply more of them (allegedly) using complex and risky structures. To be sure, this is a worst-case scenario and one we don’t see on the horizon—comments about 'cockroaches' in the credit markets notwithstanding. There was nowhere for an investor to hide in 2008, but the best managers of private credit weathered even that storm. Today’s forecast calls for selectivity rather than panic.

Now, consider the plight of the investor. As asset managers seek to “diversify their client base” away from institutions, you—dear reader—are the target for their excess supply. And their incentives are terrible: the largest managers of private assets are publicly traded companies whose stock prices respond to volume more than performance. Highly compensated sales forces blanket the country pitching stories to investment advisors (including us), even as their story becomes yesterday’s news.

So buy your umbrellas when it’s sunny and beware the “democratization” of anything financial. An investor should always ask: “why should I be so lucky and who’s on the other side?” We invite you to revisit our piece, The Velvet Rope, which lists both the opportunities and the pitfalls of investing in these markets. To summarize:

- Businesses sometimes need more of our money: more demand means better opportunities for investors.

- Lenders sometimes have more money to lend: more supply means worse opportunities for investors.

- Asset managers always want your money: the best ones will ask for it only when their (and your) opportunities are better.

- Markets adapt: try not to miss the sales and beware the bargain bin.

We watch this space closely and monitor the broader supply and demand currents in financial markets. Opportunities and risks are in constant flux. We would be delighted to share our current outlook with you in more detail, so please don’t hesitate to reach out.

*As of February 2026, credit markets have sniffed out the threat to software businesses posed by artificial intelligence. A flood of companies in this sector created record demand for both equity and credit—naturally met by supply—leading to risky industry concentration in many credit portfolios.

Disclaimer: The opinions voiced and information provided in this document is for informational and educational purposes only. It should not be considered investment, financial, or legal advice. Nothing herein constitutes a recommendation to buy, sell, or hold any security or financial instrument. Magnolia Private Wealth does not provide tax, legal or accounting advice. Investing involves risk, including the potential loss of principal. You should consult with a qualified financial advisor, tax professional, or other appropriate professional before making any financial decisions. The author and publisher assume no liability for any losses or damages resulting from the use of this information.

Insights from Our Team.