From the Frontier: Long/Short Extensions

Tax-loss harvesting is a useful strategy, but it has a natural limit. When markets are doing well, there simply aren't many losses to find. The tool that once helped reduce your tax bill gets quieter every year. Not because anything went wrong, but because a strong market doesn't give you much to work with.

Long/short extensions work on a different principle. They produce tax losses continuously, in good markets and bad, while the portfolio is still designed to grow. For investors sitting on a large gain from a stock they've held for years, a business sale, or a real estate transaction, that matters. The losses this strategy generates can offset those gains directly, often eliminating a tax bill that would otherwise be unavoidable.

What They Are

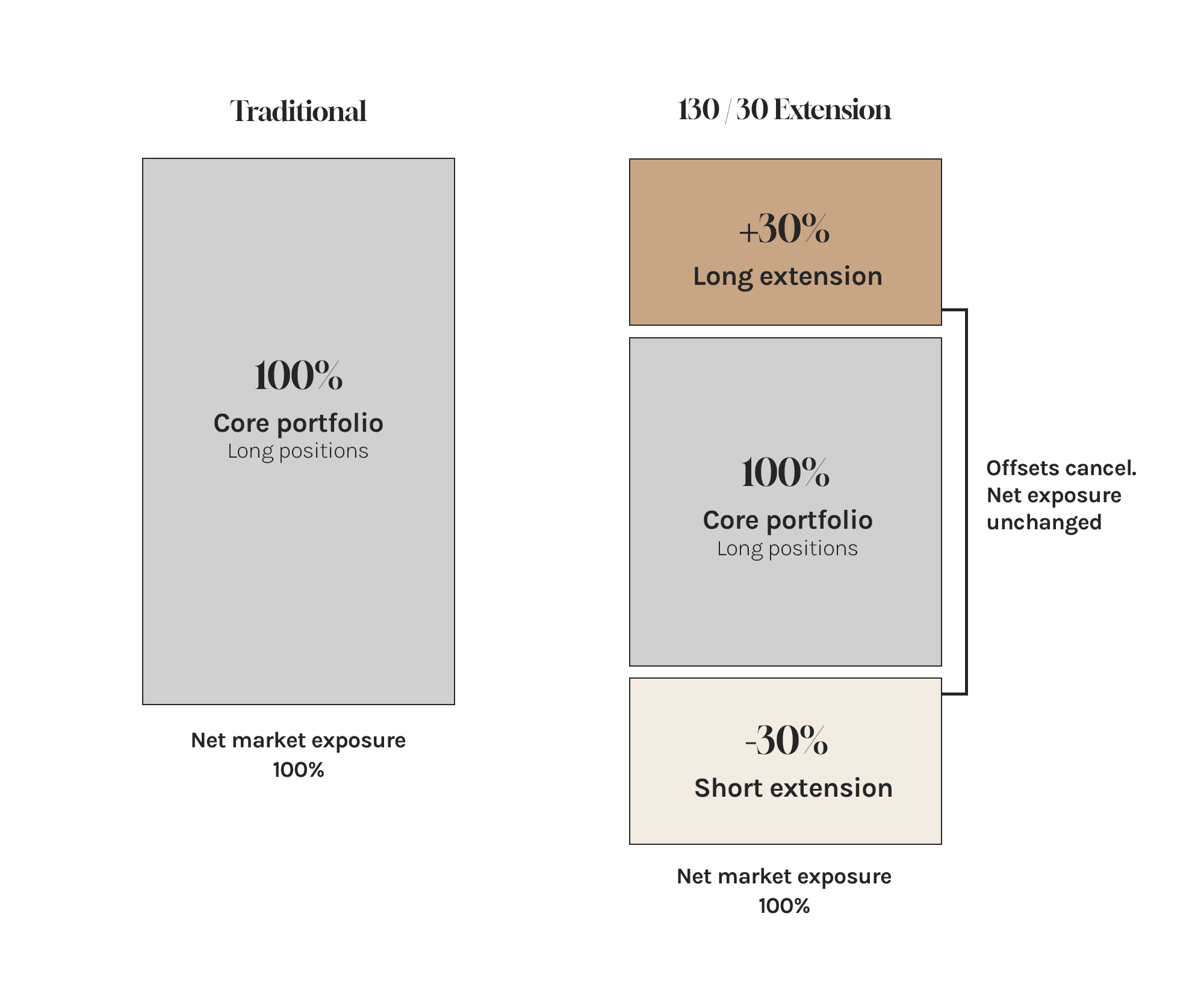

A long/short extension is an overlay added to your existing portfolio or new cash, run by institutional investment managers who have operated long/short equity strategies for decades and oversee tens of billions of dollars. The extension itself holds two types of positions: long positions in stocks the manager expects to rise, and short positions against stocks the manager expects to fall. Those two sides balance each other out, so your overall exposure to the market stays the same. You are still fully invested.

A common starting configuration, which can be referred to as 130/30, means that for every $100 of market exposure, the portfolio holds $130 in long positions, which may include your existing holdings, and $30 in short positions against stocks the manager expects to underperform, all relative to a broad market index like U.S. or global equities. The net is still $100 of market exposure. The extension can be sized larger or smaller depending on how many losses you need to generate and how much variation from the index you are comfortable with. Larger extensions produce more losses and more opportunity to beat the market, but they also cost more and will diverge more from the index in any given year.

In a traditional portfolio, you can only harvest a tax loss when a stock falls. A short position flips that. When a shorted stock rises in price, that short position loses money, and that loss can be harvested. The result is a strategy that produces tax losses in rising markets and falling ones, without any actual damage to your portfolio's value or market exposure.

The process runs systematically. The managers rank the entire universe of publicly traded stocks on characteristics like value, momentum, quality, and earnings consistency. They go long the strongest and short the weakest. Because individual stock prices move constantly and independently, there is always a fresh supply of positions sitting on losses. Those positions are sold, the loss is captured, and a similar position is opened to maintain the market exposure. The strategy runs continuously and does not require a down market to work.

The Tax Benefit

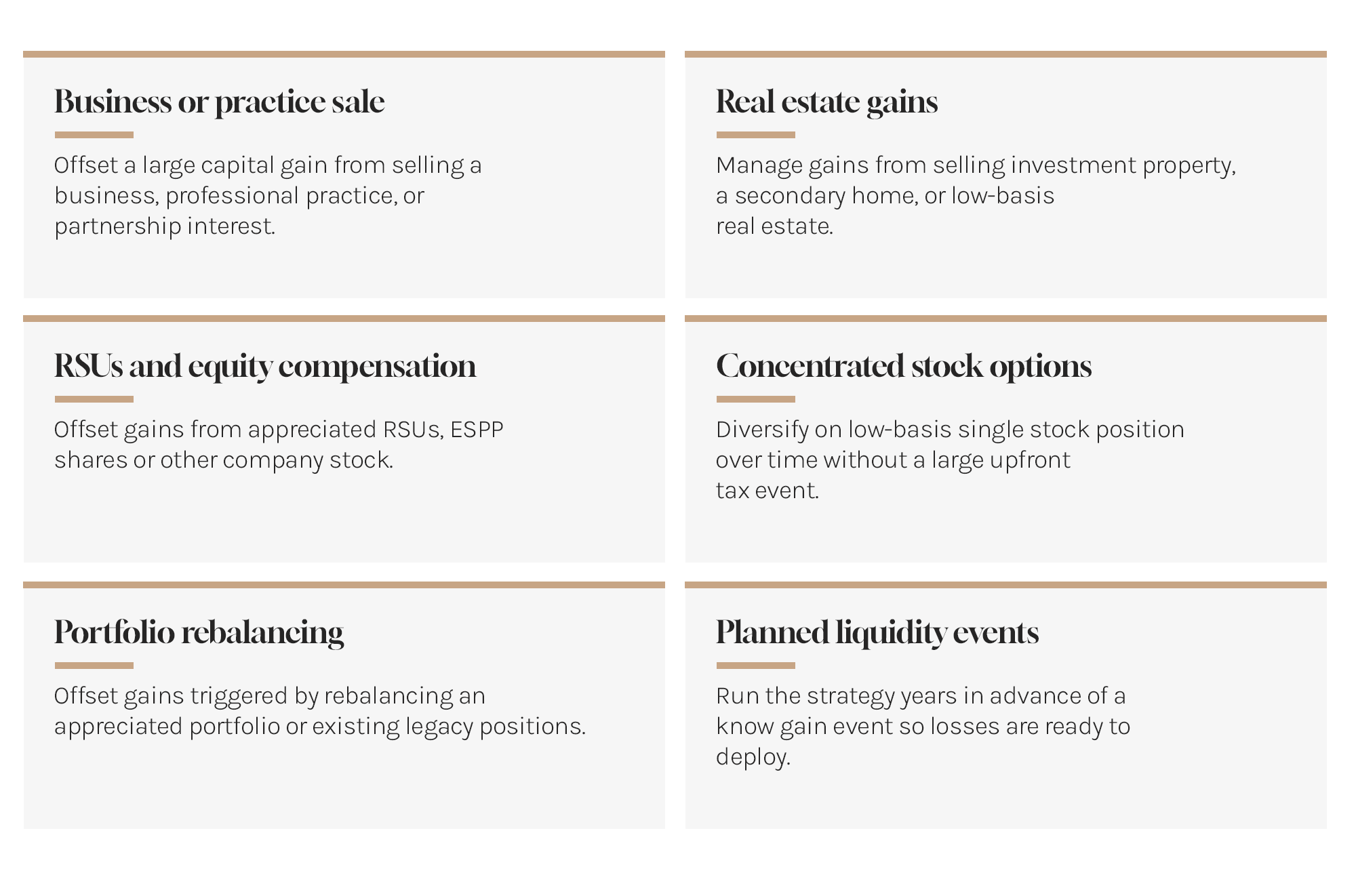

What the strategy produces, by design, is realized capital losses. Those losses offset capital gains dollar for dollar on your tax return. The goal is to generate tax losses and returns above the market, not economic losses in your portfolio. Those losses can be applied in a number of ways:

Common Applications

Specifically, the losses generated are mostly short-term and offset short-term gains first. Those gains would otherwise be taxed at ordinary income rates, up to 40.8% at the federal level including the net investment income tax. Remaining losses offset long-term gains, which are taxed at up to 23.8%. State taxes push both rates higher.

Losses that exceed your total gains in a given year can offset up to $3,000 of ordinary income and carry forward indefinitely with no expiration. Every dollar of tax deferred stays in your portfolio compounding rather than going to the IRS. And for assets held until death, a step-up in basis can turn a deferred tax into no tax at all.

The strategy produces the most losses in the early years but continues generating them consistently over time. That means the right time to start is well before you need them. A business sale, a property transaction, or a large liquidity event may be years away. The losses accumulate and carry forward, so when the gain arrives the offset is already there. Over time, those banked losses can also fund tax-efficient withdrawals from the portfolio, taking money out each year without creating a tax bill.

What it Costs and What You Get Back

These strategies come with real costs: margin interest on the additional long positions, stock borrowing fees on the short side, and manager fees. All in, a standard 130/30 typically runs 0.75 to 1.0% annually depending on the manager and the size of the extension. The interest expense is tax deductible, which reduces the net cost meaningfully for investors in high tax brackets.

Unlike passive strategies, the managers we work with apply active stock selection on both sides of the portfolio, with the goal of generating returns above the market index. That excess return is designed to more than cover the cost of the strategy over time, before you even account for the tax benefit.

Tracking Error and Risk

Active management means the portfolio will not track the index exactly. At a standard 130/30 with 1.5% tracking error, if the market returns 12% in a given year, the portfolio will likely return somewhere between 10.5% and 13.5%. At higher extension levels that range widens, as does the potential to outperform and the tax benefit.

Some years the active positioning helps. Some years it doesn't. That variability is a cost of the strategy, and one we believe the outperformance should more than offset over time.

Unwinding a Long/Short Extension

Long/short extensions are designed to deliver long-term economic value. Over time, the extension itself builds up gains of its own, the same way any long-held investment does. When it comes time to reduce or exit, how it is done matters. Wound down gradually over several years, the manager can use ongoing losses and accumulated carryforwards to offset those gains as positions are closed, returning capital to you with little or no tax bill. If unwound hastily, a large gain gets realized all at once and much of the tax benefit disappears. Larger extensions need more runway to exit cleanly, and that should factor into your decision at the onset.

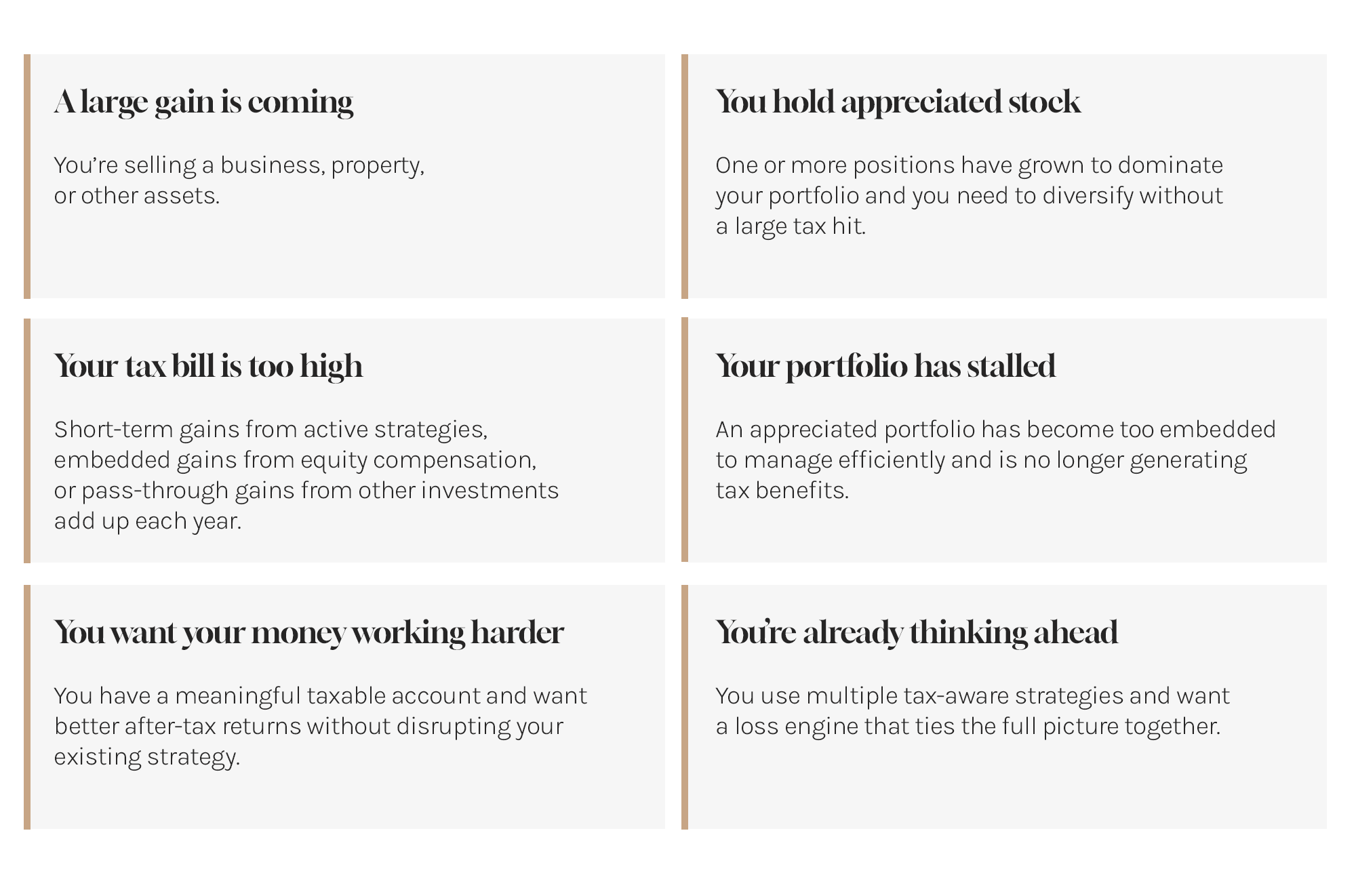

Who This Is For

Long/short extensions are not the right tool for every investor. The strategy requires a taxable account large enough to fund it, a comfort level with some degree of active management, and the ability to source liquidity from elsewhere if needed. For the right investor, the applications are broad.

Many of our clients use multiple strategies from the Frontier of Tax-Aware Investing. For those clients, long/short extensions typically serve as the foundation, generating the realized losses that allow each strategy to work more efficiently and the combined tax benefits to build over time.

Investors with substantial taxable assets tend to have capital gains in multiple places. Those gains are rarely being managed as efficiently as they could be. These strategies generally require a minimum account size of $1,000,000.

How It Works in Practice

These strategies are held in individually managed accounts in your name at a major custodian like Fidelity or Schwab. Every position is visible, every tax lot is tracked, and losses are reported on the same Form 1099 you receive each year. It is straightforward for both you and your accountant at tax time.

Magnolia's Advisory Role

Getting real value from this strategy depends on how it is implemented. Which assets fund it, how large an extension to run, which capital gains events to plan around, and how all of it fits into your broader tax picture and financial plan. That coordination is where most of the value is created or lost.

We have spent considerable time vetting managers, working through the mechanics, and running these strategies for clients. We can tell you directly whether it makes sense for your situation and how to proceed if it does.

If you are sitting on a meaningful unrealized gain, expecting a significant taxable event, or simply want to know whether your portfolio is working as hard as it could after taxes, we would welcome the conversation.

Disclaimer: The opinions voiced and information provided in this document is for informational and educational purposes only. It should not be considered investment, financial, or legal advice. Nothing herein constitutes a recommendation to buy, sell, or hold any security or financial instrument. Magnolia Private Wealth does not provide tax, legal or accounting advice. Investing involves risk, including the potential loss of principal. You should consult with a qualified financial advisor, tax professional, or other appropriate professional before making any financial decisions. The author and publisher assume no liability for any losses or damages resulting from the use of this information.

Insights from Our Team.